(Ultra Expanded Definitive Edition – 2026)

Why legal structure is now a competitive advantage in U.S. construction

The legal structure of a construction company in 2026 is no longer just about compliance. It is about access. Access to better clients, access to financing, access to bonding, access to public bids, and access to larger projects. Builders who treat licensing, permits, EIN registration, and insurance as administrative formalities often discover too late that these elements are the gatekeepers of growth. In today’s environment, compliance is infrastructure.

Construction is one of the most regulated industries in the United States. Unlike digital businesses or consulting firms, builders operate inside a layered framework of federal, state, county, and city oversight. Each layer has authority over different aspects of your operations. Ignoring one layer does not protect you from the others. The result is a system where incomplete legal setup creates hidden fragility.

Clients, especially commercial and institutional owners, now perform due diligence before awarding work. They verify license status, insurance limits, entity standing, and sometimes beneficial ownership reporting. If something looks inconsistent, approvals stall. In competitive markets, stalled approvals mean lost contracts. Legal readiness has become part of the sales process whether builders acknowledge it or not.

The companies that win consistently are not just good at building. They are structurally organized. Their documents are aligned. Their registrations are current. Their insurance certificates are clean. Their compliance posture signals maturity. That perception directly affects negotiation leverage, pricing confidence, and long-term positioning.

Federal level: the legal foundation every U.S. construction company must secure

The federal layer includes your business entity recognition with the IRS, your Employer Identification Number (EIN), tax compliance obligations, potential BOI reporting requirements under FinCEN, OSHA federal safety standards, and federal contractor registration if you intend to pursue public work. These elements shape how your company is recognized nationally.

Many builders assume the federal layer is simple because there is no “federal contractor license.” That assumption is dangerous. The IRS, FinCEN, OSHA, and SAM systems do not overlap administratively, but they overlap legally. A failure in one area can affect banking, bonding, payroll, or eligibility for public projects.

The federal foundation must be secured before scaling. Trying to fix EIN structure, payroll classification, or beneficial ownership filings after growth introduces audit risk and operational instability.

Business entity formation and federal recognition

Although business entities are formed at the state level through the Secretary of State, federal recognition becomes operational the moment you engage with the IRS. Once your entity is formed, it must align with federal tax classification and reporting standards. This includes choosing how your LLC or corporation will be taxed and ensuring that ownership information is accurately recorded.

Consistency is critical. The exact legal name registered with your state must match the name used on your EIN application, bank accounts, insurance policies, and contracts. Even minor variations create friction during underwriting, audits, or permit reviews. Builders frequently lose time correcting small discrepancies that could have been avoided during formation.

If you operate across multiple states, you may register as a foreign entity in additional states. However, your EIN remains federally consistent. This means your federal identity must remain stable even when your state footprint expands.

From a strategic standpoint, your entity structure influences liability exposure, tax treatment, and bonding eligibility. Many small builders default to LLC status without evaluating S-corp election or long-term tax implications. While the legal structure itself is state-driven, its federal tax treatment becomes central to financial scalability.

Builder Inteligence

Obtaining your EIN: the core federal identifier

The Employer Identification Number is issued by the Internal Revenue Service and functions as the Social Security number for your business. It is required to hire employees, open business bank accounts, apply for certain licenses, file tax returns, and issue payroll documentation. Without an EIN, your construction company cannot operate as a scalable legal entity.

Builders can apply directly through the IRS official website. The online application system provides immediate issuance when eligibility requirements are met. The application requires accurate business formation data, ownership details, and responsible party information. Errors at this stage propagate into tax filings and payroll systems.

The EIN is not optional if you plan to hire workers, operate under an LLC or corporation, or separate personal and business finances properly. Even sole proprietors who initially operate under an SSN often transition to an EIN to protect identity security and professionalize operations.

In 2026, many lenders, insurance carriers, and bonding companies require EIN confirmation as part of underwriting. Treating the EIN as a formality underestimates its central role in your operational infrastructure.

Federal tax responsibilities for construction companies

Once your EIN is issued, federal tax obligations begin immediately. Construction businesses must determine whether they will operate with employees, independent contractors, or a mix of both. Each classification triggers different federal tax withholding and reporting responsibilities.

Payroll compliance includes federal income tax withholding, Social Security, Medicare contributions, and unemployment tax obligations. Misclassifying workers as independent contractors when they function as employees creates federal audit risk and significant financial exposure.

Construction companies also face industry-specific tax complexities, including revenue recognition methods and cost allocation practices. While tax strategy varies by company size, the federal compliance baseline remains mandatory.

Failing to align accounting systems with IRS expectations often creates cascading issues. Builders scaling too quickly without financial structure frequently encounter penalties that disrupt growth momentum.

BOI reporting and beneficial ownership transparency

Beginning in 2024, many companies formed or registered in the United States are subject to Beneficial Ownership Information (BOI) reporting requirements under FinCEN. Construction companies structured as LLCs or corporations may be required to report ownership and control information depending on their formation date and exemption status.

BOI reporting is designed to enhance financial transparency and reduce misuse of shell entities. For builders, this requirement is administrative but serious. Failure to file when required can result in penalties.

The reporting process involves identifying beneficial owners and, in certain cases, company applicants. Builders must verify whether their entity falls within reporting thresholds and ensure compliance within required timeframes.

As construction businesses scale and bring on partners or investors, ownership structures can change. These changes may trigger updated reporting obligations. Ignoring this layer introduces unnecessary legal exposure.

OSHA federal oversight and safety compliance

The Occupational Safety and Health Administration (OSHA) enforces federal workplace safety standards that apply directly to construction operations. While states may administer their own OSHA-approved programs, federal standards provide the baseline for safety compliance.

Construction falls under OSHA’s 29 CFR 1926 standards, covering excavation safety, fall protection, personal protective equipment, electrical safety, scaffolding, and more. Builders are responsible for understanding and implementing applicable standards.

Safety compliance is not just about avoiding fines. Insurance carriers evaluate safety records during underwriting. Bonding capacity can also be affected by poor safety history. In serious incidents, OSHA investigations become central to legal defense.

Builders who treat OSHA compliance as a structured system — including training documentation, jobsite audits, and incident reporting protocols — operate with lower operational risk and stronger credibility.

Federal contractor registration and SAM.gov

For builders pursuing federal contracts, registration in the System for Award Management (SAM.gov) is mandatory. SAM registration provides a Unique Entity Identifier (UEI) and enables eligibility for bidding on federal projects.

Even builders who primarily operate in private markets should understand SAM registration if long-term growth includes public work. Registration requires accurate entity information, tax details, and compliance representations.

Federal contracting introduces additional compliance layers, including wage standards and reporting requirements. While not mandatory for all builders, SAM readiness can position a company for diversification and stability during private market downturns.

Strategically, federal readiness expands opportunity pools. Builders who delay this setup until a bid opportunity appears often miss deadlines due to incomplete registration.

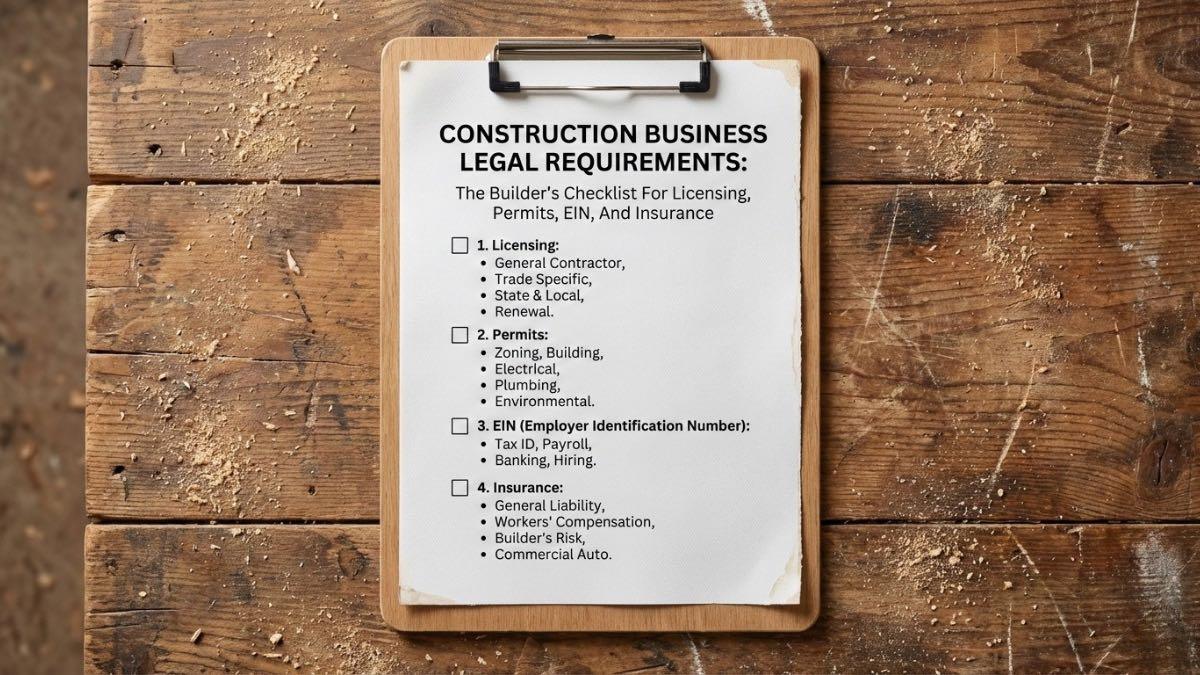

Federal level checklist summary

At the federal level, every U.S. construction company should confirm:

– EIN issued and verified;

– Federal tax structure aligned with business model;

– Payroll and worker classification compliant;

– BOI reporting obligations reviewed and filed if required;

– OSHA compliance framework implemented;

– SAM registration completed if pursuing federal work.

When these elements are secure, your company has a stable national identity. That identity supports licensing, insurance underwriting, bonding, payroll expansion, and interstate operations.

State-level licensing & registration: where legality becomes operational

State-level contractor licensing determines whether you can legally contract work, advertise certain services, pull permits, and sign binding agreements. In most serious construction markets in the United States, state contractor licensing is not symbolic — it is enforceable and traceable.

Each state defines contractor classifications differently. Some states license General Contractors at the state level. Others regulate primarily through counties or cities. Many states have strict specialty trade licensing for electrical, plumbing, HVAC, and mechanical work. Builders must identify not only whether a license is required, but which classification matches their scope.

The mistake most small contractors make is assuming “LLC registration” equals construction authorization. It does not. Business formation creates a company.

Contractor licensing authorizes construction activity. These are separate systems. Separate boards. Separate approvals. Separate enforcement mechanisms.

If you bid or advertise work requiring a license without holding the proper classification, penalties can include fines, stop-work orders, inability to enforce contracts, and even criminal liability in certain jurisdictions.

Understanding how state contractor licensing systems work

State contractor licensing boards generally operate under a Department of Professional Regulation, Department of Licensing, or similar administrative agency. These boards control:

– License classifications

– Examination requirements;

– Experience verification;

– Financial responsibility standards;

– Bond requirements (if applicable);

– Background checks;

– Renewal cycles.

Most states publish contractor requirements on official government websites under the Contractor Licensing Board or Construction Industry Licensing Board.

To determine your requirements, you must:

1. Search “[State Name] Contractor Licensing Board”

2. Identify whether your scope falls under General Contractor, Residential Contractor, or Specialty Trade

3. Review classification definitions carefully

4. Confirm whether projects above a certain dollar threshold require licensing

Many states impose thresholds. For example, projects exceeding a specific contract value may require licensing even if smaller work does not. These thresholds vary widely.

Builders who fail to review thresholds properly often discover licensing requirements only after a permit rejection.

Experience requirements and qualification criteria

Most states require proof of experience before issuing a contractor license. This is often measured in years of verifiable field or supervisory experience. In many states, applicants must show:

– 2 to 4 years of construction experience

– Experience in project management or supervision

– Documented work history

– Employer verification

– Tax documentation supporting activity

Some states allow a qualifying individual to obtain the license on behalf of the company. This person must meet experience and examination standards. If that qualifying individual leaves the company, the license may become invalid unless replaced properly.

This creates strategic implications. Builders scaling their company must understand whether their license is tied to a person or to the entity independently.

Financial responsibility is also frequently required. Some states request:

– Credit checks;

– Financial statements;

– Minimum net worth;

– Proof of insurance;

– Surety bond documentation.

Failing financial review can delay licensing approval, which in turn delays business expansion.

Contractor license examinations and testing

Many states require contractors to pass exams before approval. These exams often include:

– Business & Law portion;

– Trade-specific portion.

The Business & Law section typically covers contract law, lien law basics, labor rules, financial management, and project management standards.

Trade sections test technical knowledge specific to scope, such as:

– Structural framing;

– Mechanical systems;

– Electrical code;

– Plumbing code;

– Roofing systems;

– Concrete practices.

Exams are often administered through third-party testing vendors approved by the state board. Builders must schedule and pass exams before submitting final license approval paperwork.

Preparing for these exams is not optional. Many contractors fail on first attempts because they underestimate the business law portion. In reality, licensing exams are designed to ensure contractors understand legal and financial risk — not just how to build.

Background checks and fingerprinting

In numerous states, contractor license applicants must undergo:

– Criminal background checks;

– Fingerprinting;

– Disclosure of prior legal actions.

This is not automatic disqualification in most cases. However, non-disclosure can create serious consequences.

State boards evaluate:

– Fraud history;

– Financial crimes;

– Prior license suspensions;

– Construction-related violations.

Transparency during application is essential. Attempting to conceal prior issues can result in denial or revocation.

Builders who have moved across states must also disclose prior licensing history, including suspensions or disciplinary actions.

Reciprocity and multi-state operations

Contractors operating in multiple states must evaluate reciprocity agreements. Some states allow contractors licensed in one state to obtain licensure in another without retaking exams, provided certain criteria are met.

However, reciprocity is not universal. It may apply only to specific classifications or may exclude financial responsibility reviews.

Multi-state expansion requires:

– Foreign entity registration in the new state

– Separate contractor license application

– Local tax registration

– Insurance adjustments

Many growing construction companies underestimate the compliance complexity of interstate expansion. Licensing reciprocity reduces friction, but it does not eliminate regulatory obligations.

Builders expanding into high-growth states such as Texas, Florida, Arizona, Tennessee, or North Carolina should plan licensing well in advance of project pursuit.

License maintenance, renewal, And continuing education

Obtaining a contractor license is not a one-time event. States require:

– Periodic renewal (annually or biennially);

– Renewal fees;

– Continuing education (CE) hours;

– Updated insurance documentation;

– Bond maintenance.

Continuing education requirements vary widely. Some states require several hours per renewal cycle, often including mandatory ethics or business management components.

Failure to renew on time can result in:

– License expiration;

– Inability to pull permits;

– Administrative penalties;

– Reinstatement fees.

Professional builders create compliance calendars tracking renewal dates and CE requirements.

State-level checklist summary

Every construction company must confirm the following at the state level:

– Proper contractor classification identified;

– Application submitted to official state licensing board;

– Experience documentation verified;

– Exams passed (if required);

– Background check completed;

– Financial responsibility approved;

– Bond secured (if required);

– License active and publicly verifiable;

– Renewal schedule tracked.

State licensing is where legitimacy becomes enforceable. Without it, growth stalls.

Local / County / City-Level registration and permitting: where projects actually move or stop

If federal compliance gives your company identity and state licensing gives you authority, local registration and permitting determine whether your projects actually begin. This is the layer that affects schedule, cash flow, inspections, and client trust more than any other. Many contractors believe once they are licensed at the state level, they are cleared to operate everywhere inside that state. That assumption is one of the most expensive mistakes in construction.

Cities and counties often require separate contractor registration before issuing permits. In many jurisdictions, even fully licensed state contractors must complete municipal registration, submit proof of insurance, and pay local registration fees before pulling permits. Without this registration, permit applications are rejected automatically.

Local compliance is also where documentation consistency is tested. Permit offices compare your contractor license number, business name, insurance certificates, and contact details. If any element does not match exactly, the application is delayed. Delays compound quickly.

Inspections shift. Subcontractors reschedule. Owners grow impatient. What seemed like a minor administrative oversight becomes a project disruption.

Professional builders treat local compliance as an operational system rather than a reactive task. They prepare documentation in advance, maintain updated insurance certificates, and understand inspection sequences in their primary jurisdictions. This preparation shortens approval timelines and builds reputation with permit officials.

Business tax receipts and local contractor registration

In many cities, contractors must obtain what is commonly called a Business Tax Receipt, Occupational License, or local business registration certificate before performing work. The terminology varies by municipality, but the concept is consistent: the city wants to recognize your company as authorized to operate within its limits.

To obtain local registration, builders typically must submit:

– State contractor license verification;

– Certificate of general liability insurance;

– Workers’ compensation documentation or exemption;

– Government-issued identification;

– Application form and fee.

Some cities require in-person submission. Others allow digital upload through online permit portals. Larger jurisdictions often integrate contractor registration into electronic permitting systems. Smaller cities may rely on manual paperwork.

Builders expanding into multiple cities within the same state must understand that each municipality may have separate requirements. A company registered in one city may not automatically be authorized in the neighboring city. Overlooking this creates unnecessary permit rejection and schedule delays.

Local registration is often annual. Failure to renew may not be immediately obvious until a permit application is denied. Maintaining a renewal calendar prevents disruption.

Understanding permit systems and inspection cycles

Permits are not uniform across the United States. Some jurisdictions use advanced digital systems with online tracking, plan review comments, and inspection scheduling portals. Others operate partially on paper. Builders must understand how their local system works before promising timelines to clients.

The permit process generally includes:

– Plan submission;

– Plan review;

– Corrections (if required);

– Fee payment;

– Permit issuance;

– Required inspections;

– Final approval.

Inspection sequences are critical. Structural inspections must occur before drywall. Electrical rough inspections must precede cover-up. Mechanical inspections follow their own timeline. Missing or failing inspections can result in stop-work orders.

Professional builders map inspection timelines during pre-construction planning. They coordinate subcontractors around inspection windows rather than reacting after delays occur.

Understanding inspection requirements in your city reduces idle time and improves scheduling reliability.

Permit offices also track contractor history. Repeated violations, failed inspections, or unpermitted work can create scrutiny. Builders with clean inspection records often experience smoother review cycles over time.

Stop-work orders and enforcement risk

Local authorities have the power to issue stop-work orders when contractors operate without permits or violate code requirements. A stop-work order halts construction immediately. In severe cases, penalties and fines may accompany the order.

Stop-work events damage more than schedules. They damage reputation. Clients lose confidence quickly when projects are visibly halted. Inspectors often report repeat offenders to state boards, creating layered consequences.

Operating without required permits also exposes contractors to legal vulnerability. If a dispute arises on an unpermitted project, enforcing payment can become complicated. In some states, contractors performing work without proper licensing or permitting may lose the ability to enforce contracts.

Avoiding enforcement risk requires discipline. Builders must confirm permit requirements before starting work, even for smaller scopes. Assuming “minor work doesn’t need a permit” is a common and costly mistake.

Managing subcontractor compliance at the local level

General contractors bear responsibility not only for their own compliance but also for the compliance of subcontractors. Many municipalities require proof that subcontractors are properly licensed and insured before allowing them to perform work under a permit.

This includes verifying:

– Subcontractor license status;

– Insurance certificates listing correct classifications;

– Workers’ compensation coverage;

– City registration (if required).

If a subcontractor fails inspection or lacks required documentation, the general contractor often absorbs the delay and liability. Professional builders implement subcontractor onboarding systems to verify compliance before project mobilization.

Maintaining organized subcontractor documentation also simplifies audit processes and protects against claims. In high-value projects, owners frequently request confirmation that all trades are licensed and insured appropriately.

Local-level checklist summary

At the city and county level, every builder should confirm:

– Local business registration completed;

– Business Tax Receipt active (if required);

– Contractor registered within municipal permit system;

– Insurance certificates submitted and approved;

– Inspection sequence understood;

– Subcontractor compliance verified;

– Renewal dates tracked;

– No outstanding violations or unpaid permit fees.

Local compliance is operational control. It determines whether projects flow smoothly or stall unexpectedly.

Next we move into Insurance & Bonding Infrastructure — the financial protection layer that determines whether your company survives claims and qualifies for serious work.

Insurance & bonding infrastructure: the financial shield behind every legitimate builder

Insurance and bonding are not administrative expenses. They are structural safeguards that determine whether a construction company survives adversity. In 2026, serious clients do not ask whether you are insured. They assume you are. The real question becomes whether your coverage structure matches the risk profile of your projects.

Construction is inherently high-risk. Property damage, bodily injury, jobsite accidents, subcontractor disputes, defective work allegations, and vehicle incidents are part of the operational landscape. Insurance exists to absorb these shocks. Without it, one incident can erase years of progress.

Professional builders design insurance coverage strategically. They do not simply purchase the minimum required policy. They align policy limits, endorsements, and exclusions with the type of work performed, contract requirements, and long-term growth plans. Insurance underwriting is also a credibility filter. Companies with clean safety records and structured operations often receive more favorable terms.

Bonding operates in parallel. Bonds are not insurance for the contractor. They are guarantees to the project owner. Understanding this distinction is critical for growth.

General liability insurance: the baseline protection

General liability insurance is the foundation of construction coverage. It protects against third-party bodily injury claims and property damage claims arising from business operations. Most commercial clients require proof of general liability before awarding contracts.

Coverage limits matter. Many small contractors carry minimal limits without realizing that larger commercial projects often require higher aggregate coverage. Inadequate limits can disqualify bids automatically.

General liability policies include important elements:

– Per occurrence limits;

– Aggregate limits;

– Products-completed operations coverage;

– Additional insured endorsements;

– Waiver of subrogation clauses.

Builders must understand additional insured endorsements in particular. Many contracts require the contractor to list the owner and sometimes lenders as additional insureds. Failure to structure policies correctly can breach contract terms.

Policy exclusions must also be reviewed. Some policies exclude certain types of work or subcontracted labor. Builders who do not examine exclusions may discover uncovered exposures after a claim occurs.

Workers’ compensation: workforce risk management

Workers’ compensation coverage is mandatory in most states when employees are present. Even in states where exemptions exist for certain ownership structures, workers’ compensation remains a critical protection tool.

Workers’ comp covers medical expenses and wage replacement for employees injured on the job. Construction environments present elevated injury risk due to heights, heavy equipment, electrical exposure, and excavation hazards.

Classification codes determine premium rates. Misclassification of employees can result in costly audits and back charges. Builders must ensure payroll is categorized accurately according to trade activities.

Many commercial clients require certificates proving active workers’ comp coverage before allowing contractors on site. Even when subcontractors claim exemption, general contractors must verify documentation to avoid liability exposure.

Workers’ compensation also influences experience modification rates (EMR). A high EMR can increase insurance premiums and reduce competitiveness in public bidding environments.

Commercial auto insurance: protecting mobile operations

Construction companies rely heavily on vehicles. Trucks transport materials, crews move between sites, equipment is hauled across jurisdictions. Personal auto policies rarely provide adequate coverage for business operations.

Commercial auto insurance protects against accidents involving company-owned vehicles used for business purposes. It covers bodily injury, property damage, and sometimes cargo or equipment inside vehicles.

Builders must evaluate whether their operations trigger federal Department of Transportation requirements. Transporting certain materials or crossing state lines with specific vehicle weights can introduce additional compliance obligations.

Claims involving vehicles can escalate quickly due to bodily injury exposure. Ensuring adequate limits is not optional in today’s legal climate.

Advertising

Builders risk and project-specific coverage

Builders risk insurance covers property and materials during construction. Depending on contract terms, either the owner or contractor may carry this coverage.

Builders risk policies protect against:

– Fire;

– Theft;

– Vandalism;

– Weather damage;

– Certain structural losses during construction.

The responsibility for builders risk should be clearly defined in contracts. Assuming the owner has coverage without verification can create major exposure.

Project-specific policies are particularly important in larger commercial builds. They protect not just materials, but the progress value of work completed.

Umbrella and excess liability: extending protection

Umbrella insurance extends coverage beyond base general liability and auto limits. Many commercial and institutional clients require higher limits than standard policies provide.

An umbrella policy activates when underlying policy limits are exhausted. In serious injury cases or major property damage events, this extended coverage becomes essential.

Carrying umbrella coverage can also strengthen your competitive position. It signals financial maturity and reduces client risk perception.

Bonding: performance, payment, and license bonds

Bonds are fundamentally different from insurance. While insurance protects the contractor, bonds protect the project owner.

Common bond types include:

– License bonds (required for licensing in certain states);

– Bid bonds (guaranteeing seriousness of a bid);

– Performance bonds (guaranteeing project completion);

– Payment bonds (guaranteeing subcontractor payment).

Surety companies underwrite bonds based on financial stability, creditworthiness, and operational history. Becoming bondable requires clean financial statements and structured accounting practices.

Bonding capacity increases as financial strength increases. Builders who maintain organized accounting systems and predictable cash flow often gain higher bonding limits over time.

Many government projects require bonding. Private commercial projects increasingly require it as well.

Insurance & bonding checklist summary

Every construction company should confirm:

– General liability active with appropriate limits;

– Workers’ compensation compliant with state law;

– Commercial auto coverage in place;

– Builders risk responsibility clarified in contracts;

– Umbrella coverage evaluated;

– Bonding capacity assessed;

– License bonds secured (if required);

– Insurance certificates organized and accessible;

– Additional insured endorsements available.

Insurance and bonding are not optional overhead. They are survival infrastructure.

Next we move to Workforce, Payroll & Labor Compliance — the layer where many construction companies unknowingly create long-term legal exposure.

Workforce, payroll & labor compliance: where most construction companies create hidden legal risk

Construction operates with a hybrid labor model. Many companies employ full-time W-2 workers while also engaging independent subcontractors. The line between employee and independent contractor is not flexible simply because it is convenient. Federal and state agencies apply tests based on behavioral control, financial control, and relationship permanence. If a worker functions like an employee but is paid like a subcontractor, the company carries audit exposure.

Misclassification creates cascading consequences. It affects payroll taxes, workers’ compensation premiums, unemployment insurance, overtime eligibility, and even OSHA recordkeeping obligations. When audits occur, agencies often look back multiple years. Builders who treat workforce structure casually often discover liability long after the work was completed and profits were spent.

Professional construction companies treat workforce compliance as a documented system. They establish written onboarding procedures, clear subcontractor agreements, payroll tracking protocols, and classification audits. This discipline protects margins and prevents enforcement disruptions that can destabilize growth.

Employee vs. independent contractor: structural classification decisions

In construction, genuine subcontractors typically maintain their own business entity, carry their own insurance, control how they perform work, provide their own tools in many cases, and contract with multiple clients. Employees, on the other hand, work under company supervision, follow company schedules, use company systems, and are integrated into daily operations.

Incorrect classification creates payroll tax exposure. Employers must withhold and remit federal income tax, Social Security, and Medicare for employees. Independent contractors receive gross payment and handle their own taxes. If a worker is misclassified, the employer may become liable for unpaid employer contributions and penalties.

Builders scaling their workforce must periodically review classification decisions. Growth often blurs boundaries. A subcontractor working exclusively for one company under strict supervision begins to resemble an employee legally, even if labeled otherwise.

Payroll infrastructure and federal reporting

Once a construction company employs workers, payroll infrastructure becomes mandatory. Payroll compliance includes federal withholding requirements, unemployment contributions, and periodic tax filings. These filings are not optional administrative details; they are legal obligations tied to your EIN and business entity.

Construction payroll also introduces overtime compliance under federal labor standards. Builders must track hours accurately. Failure to compensate overtime properly can result in wage claims, investigations, and back pay liabilities.

Professional builders implement payroll systems that integrate:

– Time tracking;

– Wage classification;

– Tax withholding automation;

– Workers’ compensation reporting alignment.

Manual payroll without system safeguards increases error risk. Even small mistakes accumulate across months and years.

Certified payroll requirements may also apply on certain public projects. While not universal, builders pursuing government work must understand prevailing wage rules and reporting structures. This introduces another compliance layer that requires structured documentation.

Workers’ compensation classification and audit risk

Workers’ compensation premiums are calculated based on payroll classification codes. Each trade classification carries different risk weighting. Construction trades typically carry higher premiums due to injury risk.

Insurance carriers conduct audits to verify payroll and classification accuracy. If payroll was underreported or workers were misclassified into lower-risk categories, carriers can issue substantial back charges.

Builders must align payroll systems with workers’ comp classifications accurately. This requires coordination between accounting, insurance providers, and operational leadership. Misalignment often occurs when companies grow rapidly without updating internal systems.

Maintaining accurate payroll and classification documentation reduces audit disruption and preserves profitability.

OSHA recordkeeping and jobsite documentation

OSHA compliance extends beyond jobsite safety practices. Certain employers are required to maintain records of work-related injuries and illnesses. Even when recordkeeping exemptions apply due to company size, safety documentation remains strategically important.

In construction, incident documentation becomes essential when claims arise. Insurers, attorneys, and regulatory bodies review safety procedures, training records, and incident response logs.

Builders who maintain structured safety documentation demonstrate operational discipline. This can influence insurance underwriting, bonding evaluations, and client perception.

Safety training records, toolbox talks, hazard assessments, and site-specific safety plans form part of a protective documentation framework. Even when not mandated by specific thresholds, documentation supports risk defense.

Labor law compliance and employment policies

Beyond payroll mechanics, labor compliance includes adherence to wage standards, anti-discrimination policies, workplace safety obligations, and proper termination procedures. Construction companies operating without written employment policies increase legal exposure.

Clear documentation of:

– Hiring policies;

– Discipline procedures;

– Overtime standards;

– Safety requirements;

– Anti-harassment guidelines reduces internal conflict and protects against claims.

Construction environments involve dynamic teams and multiple trades. Clear employment structure prevents misunderstandings that can escalate into disputes.

Workforce compliance checklist summary

Every construction company should confirm:

– Worker classifications reviewed and documented;

– Payroll system aligned with federal requirements;

– Overtime tracking compliant;

– Workers’ compensation classifications accurate;

– Audit preparation documentation maintained;

– OSHA safety records organized;

– Employment policies documented;

– Subcontractor agreements standardized.

Workforce compliance is not just legal protection. It is financial control.

Next we move into Growth, Scaling & Government Readiness — where compliance transforms from obligation into competitive leverage.

Growth, scaling & government readiness: turning compliance into competitive leverage

At a certain point in every construction company’s lifecycle, compliance stops being defensive and starts becoming strategic. The builders who remain small often view licensing, insurance, payroll, and documentation as necessary burdens. The builders who scale understand that these elements become leverage — leverage for bonding capacity, leverage for financing, leverage for public bidding eligibility, and leverage for negotiating better contract terms.

Growth in construction is constrained less by skill and more by structure. A company may have strong crews, satisfied clients, and consistent demand, but without documented financial stability, clean compliance history, and scalable administrative systems, it cannot move into higher project tiers. Owners and lenders evaluate risk through documentation, not promises.

In 2026, institutional clients, commercial developers, and public agencies rely heavily on due diligence frameworks before awarding contracts. They verify license status, review insurance limits, evaluate EMR ratings, examine safety history, and sometimes request financial statements. Builders who anticipate these reviews move faster and negotiate from strength.

Compliance infrastructure also affects internal scalability. A company that tracks payroll accurately, manages insurance renewals systematically, and maintains permit-ready documentation can expand into new markets more predictably. Without these systems, growth introduces chaos rather than momentum.

Becoming bondable and increasing bonding capacity

Bonding is one of the clearest dividing lines between small-scale operators and structured contractors. Surety companies evaluate financial stability, operational history, creditworthiness, and management capability before issuing performance or payment bonds. Bonding capacity directly influences which projects a contractor can pursue.

Financial statements play a central role in bonding evaluations. Organized bookkeeping, accurate revenue reporting, controlled debt ratios, and predictable cash flow strengthen bonding applications. Builders who treat accounting casually often find bonding limits restricted.

Improving bonding capacity requires discipline:

– Maintain accurate financial records;

– Avoid excessive debt;

– Demonstrate project completion history;

– Preserve strong banking relationships;

– Keep insurance and licensing current.

Surety underwriters interpret clean documentation as lower risk. As bonding capacity increases, access to larger public and private projects expands accordingly.

Preparing for public and federal contracting

Government work introduces additional compliance layers but offers stability and scale opportunities. Federal projects require registration in the System for Award Management (SAM.gov) and assignment of a Unique Entity Identifier (UEI). State and local public projects often require vendor registration within procurement portals.

Public work may involve:

– Prevailing wage compliance;

– Certified payroll reporting;

– Bonding requirements;

– Additional insurance endorsements;

– Strict documentation timelines.

Builders who plan ahead can integrate these requirements into their operational systems rather than scrambling when a bid opportunity appears.

Public contracting readiness includes maintaining organized financial statements, safety records, license verification, and insurance documentation. Agencies often require rapid submission of compliance packets. Structured builders respond quickly and confidently.

Risk management as a growth multiplier

Growth without risk control is fragile. Construction companies face exposure from contract disputes, safety incidents, subcontractor performance issues, and payment delays. Companies that implement internal risk management protocols reduce volatility.

Key risk control elements include:

– Standardized contract templates reviewed by legal counsel;

– Documented change order procedures;

– Clear subcontractor agreements;

– Structured documentation of site conditions;

– Incident response protocols.

Builders who systematize documentation reduce disputes. When disputes arise, structured records strengthen defense positions.

Risk management also affects insurance underwriting and bonding evaluation. Companies demonstrating disciplined procedures often secure better terms and stronger capacity.

Advertising

Compliance as a marketing advantage

Most contractors treat compliance as invisible back-office work. Professional builders recognize it as a visible trust signal. Clients, especially commercial and institutional owners, respond positively to companies that present organized documentation.

Displaying:

– Active license verification;

– Insurance certificates;

– Bonding readiness;

– Safety metrics;

– Structured project documentation on proposals and digital platforms reinforces credibility.

In competitive markets, perception influences award decisions. A builder who looks organized, compliant, and financially structured often feels safer than one who appears informal — even if both have similar field capability.

Compliance, therefore, becomes part of brand positioning. It signals operational maturity.

Scaling into multi-state operations

Expansion across state lines introduces layered regulatory complexity. Each new state requires evaluation of:

– Foreign entity registration;

– Contractor license requirements;

– Local permit systems;

– Insurance adjustments;

– Workforce tax registration.

Builders who centralize compliance oversight reduce expansion friction. Creating internal compliance checklists for new markets prevents oversights that delay project starts.

Multi-state expansion also affects payroll tax obligations and workers’ compensation coverage structures. Insurance carriers must adjust policies accordingly.

Growth is sustainable only when compliance expands in parallel with revenue.

Growth & government readiness checklist summary

Every scaling construction company should confirm:

– Bonding capacity evaluated and improved;

– Financial statements organized and audit-ready;

– SAM.gov registration completed (if pursuing federal work);

– Public procurement portals registered;

– Standardized contract templates implemented;

– Risk management protocols documented;

– Compliance calendars centralized;

– Multi-state expansion reviewed carefully.

Compliance, when treated strategically, becomes the infrastructure that supports scale rather than limiting it.

Comprehensive master checklist for U.S. construction companies

To consolidate the entire guide into a unified operational framework, every builder should confirm:

Federal Layer:

– EIN issued and verified;

– Federal tax structure aligned;

– Payroll compliance active;

– BOI reporting reviewed;

– OSHA compliance structured;

– SAM registration completed if needed.

State Layer:

– Contractor license active;

– Classification verified;

– Exams completed;

– Background checks cleared;

– Renewal schedule tracked.

Local Layer

– City registration completed;

– Business tax receipt active;

– Permit documentation ready;

– Inspection sequences understood;

– Subcontractor compliance verified.

Insurance & Bonding:

– General liability adequate;

– Workers’ comp compliant;

– Commercial auto secured;

– Umbrella evaluated;

– Bonding capacity documented.

Workforce Compliance:

– Worker classification documented;

– Payroll systems structured;

– Overtime compliance active;

– OSHA documentation organized.

Growth Infrastructure:

– Risk management protocols in place;

– Financial documentation clean;

– Expansion strategy aligned with compliance.

Beyond compliance: why legal registration is only the first layer of protection

Securing licenses, registering your EIN, obtaining permits, and purchasing proper insurance are foundational legal requirements. They establish your legal right to operate. They protect you at the regulatory level. They allow you to bid, contract, and perform work without immediate compliance risk.

But compliance is not protection.

Legal registration does not stop unpaid change orders. It does not prevent subcontractor liability from shifting back to you. It does not protect against worker misclassification audits. It does not control scope creep. It does not stabilize internal workforce expectations. It does not eliminate preventable disputes.

Many contractors believe that once they are licensed and insured, their company is structurally safe. That assumption is dangerous.

Licensing gives you permission to operate.

Structure determines whether you survive.

The construction companies that scale in 2026 are not simply compliant. They are documented. They are disciplined. They have systems that prevent margin erosion before it begins.

If you have completed your legal foundation, the next step is not optional — it is strategic.

You now need internal protection.

Because the real risk does not begin at the state licensing board.

It begins inside your daily operations.

That is exactly why we built the next framework:

The builder protection system: the complete operational framework with downloadable templates for U.S. contractors

In that article, you will find the structured documentation tools that protect your subcontractor relationships, change orders, insurance verification, workforce governance, payment security, and proposal clarity.

If you are serious about building a construction company that survives market volatility instead of reacting to it —

Do not stop at compliance.

Move forward and build protection into your operations now.

Builder Inteligence

FAQ — Construction business legal requirements: the builder’s checklist for licensing, permits, EIN, and insurance

1. What are the first legal steps to start a construction company in the U.S.?

Start by choosing a business structure (LLC or corporation), registering it with your state, and getting an EIN from the IRS. Then confirm your state contractor licensing requirements, register locally where required, and secure baseline insurance. You also need compliant contracts, proper tax setup, and a system to track permits, inspections, and certificates.

A business license is a general permission to operate a company in a city, county, or state, often tied to tax registration. A contractor license is a professional or trade license that authorizes you to perform construction work under regulated standards. Many contractors need both, plus local registrations and permits depending on job location.

An EIN is a federal tax identifier issued by the IRS for your business. Contractors need it to open business bank accounts, hire employees, run payroll, file business taxes, obtain insurance, apply for licenses, and work with many clients. It also helps separate personal and business identity, which matters for liability and compliance.

You apply through the IRS, and many applicants receive an EIN immediately when using the online application, assuming the information matches IRS validation. You can also apply by mail or fax, which takes longer. Keep the confirmation letter saved because you will use it repeatedly for banking, licensing, and insurance onboarding.

No. An EIN is federal and stays with your business. However, states may require separate tax registrations, payroll accounts, unemployment insurance accounts, and licensing or registrations. Think of the EIN as your federal identity and state accounts as your operational permissions and tax obligations within each state.

Permits vary by city and county, but common categories include building permits, trade permits (electrical, plumbing, mechanical), demolition permits, and sometimes zoning approvals. Typically the licensed contractor pulls permits, but some jurisdictions allow owners to pull permits under specific conditions. Always confirm with the local building department to avoid stop-work orders.

Local permitting follows a cycle: application, plan review, permit issuance, inspections at defined milestones, corrections if needed, and final inspection for closeout. Delays usually come from incomplete documents, missing contractor registrations, insurance certificate issues, or failed inspections. A strong builder runs permitting like scheduling, with checklists, timelines, and responsibility assigned.

General liability is the baseline most clients expect. If you have employees, workers’ compensation is usually required. Many projects also require commercial auto if vehicles are used for work. Beyond that, builders risk, umbrella, and professional liability may be appropriate depending on scope. The “right” baseline depends on trade, project type, and client requirements.

Bonds are financial guarantees, commonly required on public projects and some large private jobs. Performance bonds assure completion, and payment bonds protect subs and suppliers. Some states also require license bonds. If you want to compete for bigger work, bonding readiness is part of growth planning because it affects bid eligibility and client confidence.

They often request proof of licensing, certificates of insurance, W-9, company registration details, safety documentation, references, and sometimes financial statements. On larger projects, they may request an EMR, safety program, QA/QC plan, and prior project experience. Builders who package these items cleanly win trust faster and reduce pre-award friction.

Use a simple compliance system: a master checklist by state and by city, a renewal calendar, and a shared folder with version control for licenses, insurance COIs, bonds, registrations, and templates. Set reminders for renewals at least 60–90 days in advance. Builders lose momentum when paperwork becomes reactive instead of operational.

Yes, and sometimes more. Smaller contractors have less margin for mistakes and fewer people to fix problems under pressure. A basic compliance structure protects your cash flow, prevents shutdowns, reduces disputes, and supports higher pricing. The builder who looks organized wins trust, even if the team is small.

Strong templates clarify scope, exclusions, payment terms, change order rules, schedule assumptions, material lead times, site access, responsibilities, warranty terms, and dispute resolution steps. Your contract should reflect modern risk realities like volatility and delays. Templates should be consistent with your operational process so you are not promising what you cannot control.

Multi-state operations require licensing research per state, registration tracking, tax setup, and an internal playbook. Reciprocity may help, but it is not automatic. You also must manage local permitting rules and insurance endorsements. The builders who scale safely treat compliance like estimating, with repeatable systems instead of memory and improvisation.

GEO is location-specific structuring of information so builders can match requirements to the state, county, or city where work happens. It matters because compliance is not universal. A portal that organizes requirements by market improves real-world usefulness, increases search visibility, and reduces misinformation risk. Builders search locally because enforcement and permitting are local.

Verify licensing status through the state board, confirm local registrations where required, request a certificate of insurance naming required parties when needed, and confirm worker classification alignment. Ask for W-9 and company details. Keep a subcontractor compliance checklist and require documents before mobilization. Your project risk is tied to your subs’ compliance.

Track license renewals, local registration renewals, insurance renewals, payroll filings, tax due dates, COIs for active jobs, permit status, inspection schedules, and subcontractor documentation. Also track disputes, change orders, incidents, and near-misses because they affect insurance and risk costs. Consistency monthly prevents chaos quarterly.

They miss local registration requirements, work without proper permits, have expired insurance certificates, misunderstand license classifications, or misclassify workers. Another common issue is poor documentation organization, which makes a compliant contractor look noncompliant. Builders win when they treat compliance like a system, not a one-time checklist.