The insurance framework every U.S. contractor needs to protect projects, payroll, cash flow, and long-term growth

Insurance is not a secondary requirement in the construction industry. It is one of the structural foundations that determine whether a contractor can operate safely, legally, and sustainably in the United States. Many builders focus first on equipment, licenses, crews, and contracts, but insurance often determines whether the company can actually start a project, sign a contract, or access larger opportunities in the market. In construction, insurance is not just protection — it is operational permission.

The U.S. Small Business Administration explains that business insurance protects companies from financial losses caused by accidents, lawsuits, disasters, or operational disruptions. These risks are especially relevant in industries that involve physical labor, equipment operation, and project-based contracts. Contractors work in environments where injuries, property damage, and legal disputes are realistic possibilities, which is why proper insurance coverage becomes essential for survival.

Official source explaining business insurance fundamentals:

U.S. Small Business Administration – Business Insurance Guide

https://www.sba.gov/business-guide/launch-your-business/get-business-insurance

The reality of construction is that most serious projects require insurance before work begins. Developers, municipalities, commercial property owners, and large general contractors almost always require proof of insurance in the form of Certificates of Insurance (COI). Without those documents, subcontractors and contractors are often not allowed to enter the jobsite. In other words, insurance is not just about risk management after something goes wrong. It is a gatekeeper to the market itself.

Insurance also plays a strategic role in the financial credibility of a construction company. Banks, bonding companies, investors, and project owners evaluate whether contractors maintain adequate insurance coverage before trusting them with large projects. A company that lacks proper coverage is often perceived as financially unstable or operationally risky. Builders who structure their insurance correctly not only protect themselves from legal exposure but also position their companies to access more serious opportunities.

Why insurance matters more in construction than in most industries

Construction is one of the most risk-exposed industries in the U.S. economy. Jobsites involve heavy equipment, hazardous environments, elevated work areas, electrical systems, structural modifications, and coordination between multiple trades working simultaneously. Because of this complexity, the probability of accidents or disputes is inherently higher than in many other sectors.

According to the U.S. Occupational Safety and Health Administration (OSHA), construction consistently ranks among the industries with the highest rates of workplace hazards, particularly related to falls, struck-by incidents, electrocutions, and caught-between accidents. These risks do not automatically lead to legal claims, but they illustrate why insurance protection is necessary.

Official OSHA workplace safety statistics:

Occupational Safety and Health Administration – Construction Industry Safety

https://www.osha.gov/construction

Beyond safety issues, construction companies also face contractual liability. Projects involve agreements that define responsibilities for property damage, structural defects, project delays, subcontractor performance, and warranty obligations. If something goes wrong, responsibility often becomes a legal question, and insurance helps absorb the financial consequences of those disputes.

Without proper insurance coverage, contractors may have to pay legal costs, settlements, or repair costs directly from company assets. For small and mid-size construction companies, a single serious claim can threaten the entire business.

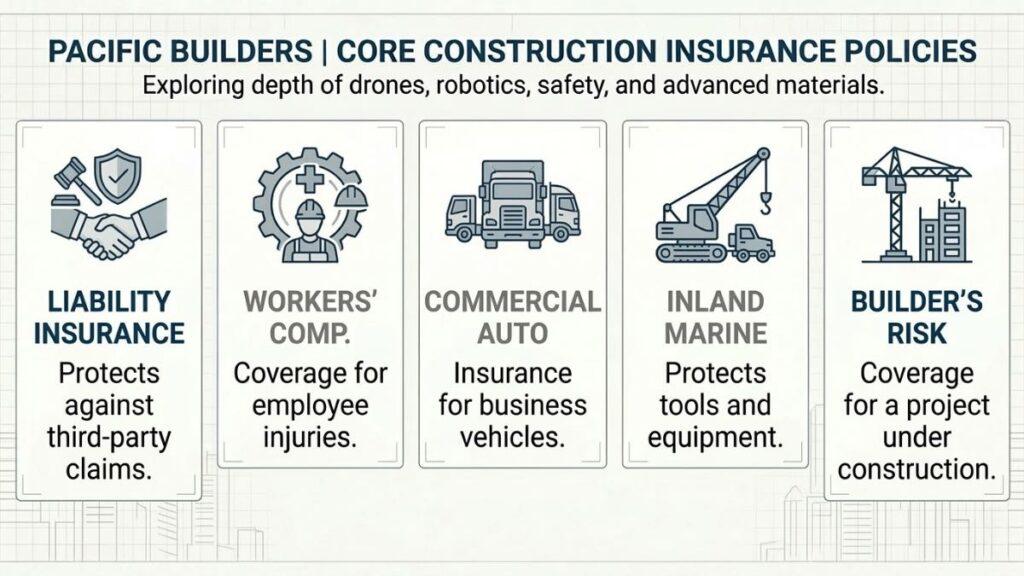

The five core insurance policies every construction company should understand

A serious contractor should understand the main insurance categories used in the construction industry. Each policy protects the company against a different type of risk exposure.

The most common construction insurance policies include:

1. General Liability Insurance

2. Workers’ Compensation Insurance

3. Commercial Auto Insurance

4. Builders Risk Insurance

5. Professional Liability Insurance

Understanding how each policy works helps contractors build an insurance framework instead of purchasing random coverage.

General liability insurance

General liability insurance is the most fundamental policy used by construction companies. It protects the business if the company causes property damage or bodily injury to third parties during the course of operations. If a contractor damages a client’s property, accidentally causes injury to a visitor on the jobsite, or creates a condition that results in financial loss for another party, general liability insurance may cover legal defense costs and damages.

Many project owners require minimum liability limits before allowing contractors to participate in a project. Typical limits in the construction industry often start at $1 million per occurrence and $2 million aggregate coverage, although large commercial projects may require higher limits.

Official overview of general liability insurance:

Insurance Information Institute – Commercial Liability Insurance

https://www.iii.org/article/commercial-liability-insurance

Workers’ compensation insurance

Workers’ compensation insurance protects employees who are injured while performing their work. Construction is a physically demanding industry, and injuries can happen even in companies with strong safety practices. Workers’ compensation helps cover medical expenses, lost wages, and rehabilitation costs for injured employees.

Most U.S. states legally require employers to carry workers’ compensation insurance once they hire employees. Requirements vary by state, but failure to carry this coverage can result in serious penalties, fines, or even business shutdowns.

State requirements for workers’ compensation:

U.S. Department of Labor – Workers’ Compensation Programs

https://www.dol.gov/agencies/owcp

Contractors who hire subcontractors should also verify whether those subcontractors carry their own workers’ compensation policies. If they do not, the hiring contractor may become financially responsible for injuries involving those workers.

Commercial auto insurance

Construction companies frequently rely on trucks, vans, and other vehicles to transport crews, tools, and materials between jobsites. Personal auto policies typically do not cover vehicles used for business purposes, which is why commercial auto insurance is necessary.

Commercial auto insurance protects contractors from liability if company vehicles are involved in accidents while performing business operations. Coverage may include property damage, bodily injury liability, collision coverage, and uninsured motorist protection.

Official explanation of commercial auto insurance:

National Association of Insurance Commissioners – Commercial Auto Insurance Guide

https://content.naic.org/consumer/auto-insurance

Even small construction companies with only one vehicle should consider commercial auto coverage because vehicle accidents represent one of the most common sources of liability claims.

Builders risk insurance

Builders risk insurance protects construction projects themselves while they are being built. This policy typically covers damage to structures under construction caused by fire, vandalism, weather events, or other unexpected incidents.

Builders risk insurance is especially important for contractors working on large projects where the structure being built represents a major financial investment. Without this coverage, damage occurring during construction could create enormous financial exposure.

Explanation of builders risk insurance:

Insurance Information Institute – Builders Risk Insurance

https://www.iii.org/article/builders-risk-insurance

Builders risk policies often expire once the project is completed and the building becomes operational.

Professional liability insurance

Professional liability insurance (sometimes called errors and omissions insurance) protects contractors against claims related to professional mistakes, design errors, or negligence in project planning or consulting services.

This coverage is particularly important for contractors who provide design-build services, engineering input, or project management consulting.

Professional liability overview:

Insurance Information Institute – Professional Liability Insurance

https://www.iii.org/article/professional-liability-insurance

Even contractors who primarily perform physical construction work may face claims related to project recommendations or technical decisions.

Why insurance helps contractors win larger projects

Insurance coverage is often a requirement in bidding processes. Many project owners will not allow contractors to submit proposals without proof of adequate coverage limits. Insurance certificates also demonstrate that the contractor operates professionally and understands risk management.

In addition, lenders and bonding companies frequently evaluate insurance coverage before providing financial backing for projects. Companies that maintain strong insurance structures often qualify more easily for credit lines, bonding capacity, and large-scale commercial contracts.

For contractors planning long-term growth, insurance should be viewed as part of strategic business infrastructure.

FAQ – Construction company insurance explained

1. Why do construction companies need multiple insurance policies instead of just one?

Construction companies face several types of risk simultaneously, including property damage, worker injuries, vehicle accidents, professional liability, and project-specific losses. Because these risks are different in nature, they are covered by separate insurance policies designed to address each exposure appropriately.

2. Is general liability insurance legally required for contractors in the United States?

General liability insurance is not always mandated by federal law, but many states, licensing boards, and project owners require contractors to carry minimum liability coverage before they can legally perform construction work or participate in project bids.

3. What happens if a contractor operates without workers’ compensation insurance?

If a contractor fails to carry workers’ compensation insurance where it is legally required, the company may face fines, lawsuits, or criminal penalties. Additionally, the contractor may be personally responsible for medical costs and wage replacement for injured employees.

4. Do subcontractors need their own insurance policies?

Yes. Subcontractors are typically expected to maintain their own liability and workers’ compensation coverage. General contractors often require proof of insurance before allowing subcontractors to work on a project to avoid financial exposure.

5. How much insurance coverage should a construction company carry?

Coverage requirements vary depending on project size, state regulations, and contract terms. Many construction contracts require at least $1 million in general liability coverage, although large commercial projects may demand significantly higher limits.

6. What is a certificate of insurance (COI)?

A certificate of insurance is a document issued by an insurance provider that verifies a contractor’s active coverage. Project owners and general contractors commonly request COIs before allowing work to begin on a project.

7. Does insurance replace safety programs on construction sites?

No. Insurance does not replace safety programs. Strong safety practices reduce accidents, lower insurance premiums, and protect workers. Insurance provides financial protection after incidents occur, while safety programs aim to prevent those incidents.

8. Can insurance help contractors qualify for larger projects?

Yes. Many developers, municipalities, and general contractors require proof of insurance before awarding contracts. Builders with strong insurance frameworks appear more credible and financially responsible, which helps them access larger opportunities.